Scroll down for updates. Inspection records available for Tippy’s Taco House owners’ previous restaurant (which is now under new ownership and management).

Typically the Winchester Watchdog focuses strictly on government issues as the author is a big fan of private enterprise. But sometimes private businesses need a dose of sunshine.

There has been quite a bit of talk around the town lately about Tippy’s Taco House. Some were just rumors, and some were newspaper reports. As WW readers are well aware, this blog does not normally engage in rumormongering… no one wants to be sued for libel after all. But some odd little bits of information in local news articles piqued this author’s interest (and admittedly some rumors about food quality did as well.)

In December 2010, Lorie Showalter reported for the Sherando Times that Terry Hudson (a previous owner of Sweet Caroline’s in Winchester) approached and eventually persuaded the franchiser to start a new Tippy’s Taco House:

He “bugged” the franchise owner for years to sell a franchise to him and she finally agreed, putting very few caveats on the new owners.

The story changed a bit in 2011.

On January 5, 2011, The Winchester Star published an article titled “Finally a Tippy’s Taco House” by Stephanie Mangino. According to the article:

New franchises of the small chain aren’t approved these days, but Hudson said one of its owners found a dormant franchise for him to take over.

In an article for Around the Panhandle magazine (April 2011), Terry Hudson is quoted as saying:

I found out they were not selling new franchises but that an existing contract was dormant. I quickly got in touch with the owner and she gave me a price I couldn’t pass up.

He also claimed that “the main focus of Tippy’s is definitely the food. Everything is fresh and made daily…”

On May 31, 2011, one reader (“TOB”) claiming to be a former employee commented on The Winchester Star‘s online article:

They lie about the food being “homemade,” in particular the salsa (which comes from Costco), the guacamole (which is bought frozen, filled with preservatives that keeps it bright green for weeks), refried beans that come from the can, etc.

Whoops.

Another reader (“Ovechkin” of Stephens City), commenting on a recent Winchester Stararticle about a lawsuit against the restaurant for lease non-payment, wrote:

if your business is named after any food you serve (ie Tippy’s TACOS) One would think the named food would actually taste somewhat decent to which the company was named. (ieTACO). I always support local businesses and went there twice… the second thinking the first was just a fluke. Not good, not good at all. So either they close now or business would force their hand. It is too bad, but if you can’t produce a quality product, then ultimatley the public will not support you.

Yelp has reviews here and here. Read Winc Food reviews here.

The health department inspection results for the restaurants are available online here.

Take ’em with a grain of salt.

Personal knowledge of Hudson’s previous kitchen management when he owned another restaurant in Winchester proved that health inspections don’t necessarily mean meat won’t sit rotting in an oven for a year because the oven doors are “welded shut” by grease and salad won’t turn to black soup in the walk-in refrigerator. (And that’s no rumor, folks.)

The “Tippy’s Taco House” trademark has a long history. It was listed as “CANCELLED-SECTION 8” on Trademarkia.com since 2001 until this spring when Locklier Company, Inc. in Texas filed a new application for the trademark. It is now listed as “NEW APPLICATION – ASSIGNED TO EXAMINER.”

It appears that in 1988, and then later in 2001, the United States Patent and Trademark Office cancelled the trademark registration since a timely Section 8 Declaration was not filed by the current owners. A Declaration of Continued Use or Excusable Nonuse under Section 8 is

a sworn statement, filed by the owner of a registration, that the mark is in use in commerce. Section 8 of the Trademark Act, 15 U.S.C. §1058. If the owner is claiming excusable nonuse of the mark, a §8 Declaration of Excusable Nonuse may be filed. The purpose of the §8 Declaration is to remove marks no longer in use from the register.

Mary Locklier is an owner of Locklier Company and the daughter of the late Jack Locklier, the originator of Tippy’s Taco House in Texas. Perhaps she is reviving the franchise. But considering the trademark had been cancelled for so many years, was there anything to “sell”?

Oddly enough, on Wednesday DallasTxBusinessLawyer.com, the website for Smith Kendall PLLC in Dallas, posted the following blog article:

Nevada Restaurant Involved in Debt Collection Litigation

Posted on Wednesday, July 27th, 2011 at 3:36 pm.

Written by admin

A Nevada restaurant is involved in a contract dispute with a Winchester landlord.

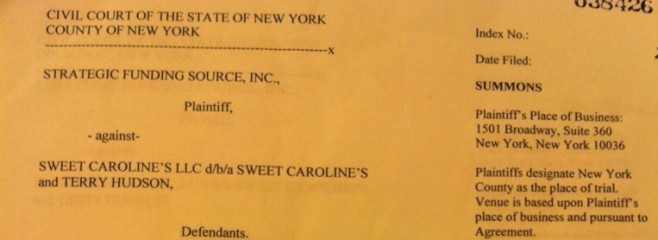

According to the lawsuit, Tippy’s Taco House in Stephens City owes rent to Jai Euk Lee and Young Sook Lee going back to 2009. The Lee’s own the property at 175 Fairfax Pike in Stephens City and have leased it to the defendant, Terry Hudson, since a lease agreement established September 3, 2009.

According to Frederick County Circuit Court documents, Hudson agreed to pay $2,000 per month until August 31, 2010; then $2,500 per month until August 2011 for the second year, and $2,750 for the third year. Hudson owes $50,530.70 in rent for December 2009 through February, plus $12,500 for March through July “if applicable,” the complaint states. The defendant also owes $4,530.70 in real estate taxes for 2010 and 2011, Lee says.

The owners say Hudson owes an undetermined amount for damages to the property. They are seeking immediate possession of the property and a court order to remove the defendant from the premises.

If a debtor is unable to pay you, securing a legal judgment against that person or company can ensure you receive the outstanding balance. The judgment will give you the right to collect payment as soon as the debtor in question has the assets to cover the debt. To speak with a Dallas Collections Lawyer, please contact Smith Kendall, PLLC, by calling 214-361-6124.

It is not clear why the lawyers group calls it a “Nevada restaurant.” The article seems very similar to this one from The Northern Virginia Daily.

Another blog post on this topic may be expected next week pending responses from Texas lawyers and franchise information groups.

UPDATE: (Aug 1 @ 10:30am) Got off the phone with the owner of a couple Tippy’s Taco Houses in northern Virginia. He is using 40-year-old Tippy’s Taco House recipes. Because the franchiser in Texas has basically retired, there is no real enforcement of Tippy’s standards or conformity. It is very lax. And so that is why food in the Winchester or Stephens City restaurants may not taste like the food at other Tippy’s restaurants.

UPDATE: (Aug 3 @ 3:00pm) Health inspection records available for Terry Hudson and Zach Vakaris’ previous restaurant Sweet Carolines LLC. Click here to download them: Health Inspection Records (Note–The restaurant was purchased and renovated by Jesse and Stephanie Levenson through their company Sweet Carolines in Winchester LLC in the summer of 2009.)

No, I am not quitting, just focusing my efforts on another city and county right now.

I believe that I have provided sufficient food-for-thought to the people of Winchester and Frederick County, and I can only hope people will continue to think and talk about these things like private property rights and cronyism in government. As it is, I think there are many strong Frederick County and Winchester residents who are unwilling to sit by quietly any longer.

As new issues arise in the Winchester area, I will likely write about them if I believe the local media is not doing a sufficient job. For now, I believe I need to pierce the incredibly non-transparent realm of West Virginia. Gun rights and strip clubs aside, that state is a haven for big government guzzlers of tax dollars and lovers of heavy-handed regulation. I will have my hands full for some time.

Editor’s Note: I just want to say that I love historic buildings and historic downtown areas like Old Town Winchester. Beautiful architecture and historic monuments can be priceless. This post should not be interpreted as “anti-rehabilitation of historic buildings” or “anti-preservation of American history.” What I did not understand until recently is what goes on behind the scenes of historic building rehabilitations and renovations. I did not know how much projects like that really cost, and I never knew who paid for them. I also never fully appreciated the expanding Historic zone and what that means for property owners and taxpayers. This article is a compilation of what I have learned about the use of historic tax credits in the City of Winchester.

Background information and how it all starts

Let’s say someone owns a house next door to historic Winchester and maintains it well. The property will appraise at a much higher value than if the building were permitted to fall into disrepair. The homeowner does not get tax credits for his continual upkeep on the house, nor does he get a break on his income taxes for maintaining his home. In fact, should he make improvements, he will have to pay higher property taxes.

His neighbor, on the other hand, lives in the Historic district and cannot afford to maintain or chooses not to maintain his historic house. The home falls into disrepair and is basically not suitable for habitation. The tax reassessment on his home will be lower. Unlike antique, well-kept cars that are exempt from higher property taxes in the City, antique well-kept homes have to pay the same property taxes as everyone else unless they qualify for real estate tax abatement. In fact, they have to pay the same tax rates while having to deal with extremely restrictive zoning ordinances and powerful local committees like the Board of Architectual Review.

Finally, the delapidated old house becomes a public nuisance due to vermin infestations and an unstable structure. The City labels it a “blight” and notifies the owner that he must submit a suitable spot blight abatement plan within a certain amount of time. The owner cannot afford to perform the necessary repairs or he chooses not to. Eventually it is likely that the property owner will either sell the property or lose it to the government who condemns the property and acquires it through eminent domain.

Sometimes it is cheaper and faster to simply demolish the old structure and build something completely new rather than attempt to renovate or rebuild using the old materials. In fact, it is probably always cheaper and faster. But suppose the government really doesn’t want to demolish the house. Let’s say it is very special to local preservationists and historians. Maybe it housed a famous person. Whatever the reason, the local government tries everything in its power to prevent demolition of the building.

This means that the more expensive route must be taken which involves acquiring the property and then rebuilding and renovating the house. Someone has to pay for it, and in order for someone in the private sector to take on a project of such magnitude and risk, typically the rewards need to be pretty lucrative. When purchasing a building in such bad disrepair, who knows what you might find as you sift through the mess, right? The investor must have the financial capital to pay a construction company to perform the work. When it comes to private sector work, most construction companies have learned that it is wisest to ask for certain costs to be paid upfront just in case the investor files for bankruptcy before the job is completed. Normally in the private sector, people would not be interested in these expensive projects except perhaps for reasons of philanthropy or personal interest in historic buildings and such. So, how do you attract someone to participate in such a project? Money.

Where the money comes from is a little complicated. We start with the government who doesn’t have the cash on hand to fund such projects but really wants to see them happen. Why they want to see them happen is also complicated–generally, though, it comes down to lobbyists. But the government has a pretty steady cash flow from income taxes, especially taxes paid by large, well-established corporations that likely aren’t going anywhere. What if the government can promise a corporation that if they rehabilitate an historic building, they won’t have to pay their $500,000 yearly income tax bill for the next 10 years? That is a lot of money the corporation gets to keep in their pockets…and the corporation will also have a valuable piece of property when it is all said and done.

But the average property owner in Frederick County is never going to pay $5M in income taxes, therefore such tax credits would not be worth the upfront cost of rehabilitating an historic building. This is where consulting firms like Brian Wishneff & Associates come in to find the big third-party investors who can actually use $5M in tax credits. As was previously discussed in the article on the Snapp Foundry building, John Willingham’s partnership was able to pay for the construction on the property with cash received by selling millions of dollars in tax credits. And until last month’s important court ruling, such a transaction was not taxed by the government as a sale.

The tax credit does not equal government spending per se, but it does mean reduced government revenue. The people directly profiting from this program are the developers and third-party investors. If government spending is not adjusted to account for the tax credits, the government will have to go further into debt or raise revenues elsewhere (ie. taxation). The average Virginia citizen is not eligible for tax credits for maintaining or rehabilitating his home or business (unless he plans on spending gobs of money “green-ifying” the property.) The average Virginia citizen is not eligible for real estate tax abatement. Historic tax credit programs are not designed for the average person. It is a market geared toward huge corporations and wealthy developers, which is understandable considering the cost to rehabilitate old buildings is very high.

Putting historic tax credits to work in Winchester

In April The Winchester Star featured an article celebrating $86.5M of private investment in the City of Winchester. (The number touted was $100M when adjusted for inflation.) What it failed to reveal was the amount of tax credits funnelled into the City for rehabilitation costs, nor did it mention the loss of real estate tax revenue thanks to the City’s tax abatement program. The idea behind the tax abatement program (which is like a local form of tax credits) is that the City will see a return on its initial investment (the loss of potential real estate tax revenue) through the revitalization of the area that is so dependent on the rehabilitation of that particular building. In other words, by giving up five years of real estate tax revenues now, the City will be so markedly improved by the rehabilitated property that new tax revenues in the form of increased sales and higher area assessment values will more than make up for the initial cost of abated real estate taxes.

But are the benefits of these rehabilitation projects worth the cost? Can monetary value be placed on aesthetics and historicity? Does the City really see a return on its investment? Do the tax credits encourage extravagance rather than efficiency and innovation? These are questions not answered by this post, but hopefully the information within it can help readers come to rational conclusions.

9 Court Square

According to Karen Helm, executive director of the Old Town Development Board, the watershed project for downtown investment seems to have been Farmers & Merchants Bank-Winchester’s renovation of seven buildings at 9 Court Square in the mid-1990s (The Winchester Star, April 12, 2011). The “Wilbur M. Feltner Building,” located just south of the Old Courthouse Civil War Museum, was dedicated in honor of the F&M Bank President and current trustee emeritus at Shenandoah University.

In 1994, Mr. Feltner announced plans to renovate the property.

According to a FY 1995 SEC document, on April 11, 1995, F&M Bank-Winchester acquired from the County of Frederick property located at 9 Court Square consisting of land and buildings in exchange for 2 parking lots of equal value:

In order to expand our downtown F&M Bank-Winchester operation, we traded property with Frederick County, Virginia, and acquired the historic Frederick County Court Square offices. These offices are now being renovated, along with a city parking lot located on North Cameron Street. We also acquired the vacant Solenberger Hardware Store building and lot. This lot, along with the city parking lot, is being made into an employee parking lot.

In the same document, a letter written to shareholders, customers and friends stated:

The land transactions that we had with Winchester and Frederick County are now complete and the renovation of 9 Court Square, which is due for completion around Labor Day, will afford us the additional space we need since we have outgrown most of our banking departments. We anticipate moving F&M Bank-Winchester’s Trust and Credit Card Departments to the new location.

The project was completed in 1997. As reported by The Winchester Star and Don Swofford FAIA, historic tax credits played a key part in the rehabilitation project of 9 Court Square, which is now valued at $3.2M. How big of a part remains to be seen–it probably requires a few phone calls. Maybe later.

On April 1, 2011, the Feltner Community Foundation announced that it would donate the 9 Court Square buildings to Shenandoah University, making it the University’s largest-ever property gift. For more information, see Shenandoah University’s article here.

Lewis Jones Knitting Mill Building

The former knitting mill building at 126 North Kent Street is now the corporate headquarters for OakCrest Builders Inc. and OakCrest Properties LLC.

In August 2005, OakCrest Cos. owner James Vickers purchased the property for $1.1M. The project development began in October 2005 and was completed in February 2007. According to Mr. Vickers, the cost of the renovation including land acquisition was $6.5M. OakCrest received $2.5M in tax credits, according to an article in The Winchester Star (Erica Bush, April 23, 2007). Frazier Associates provided full architectual services and assistance with the historic tax credit applications for the financing part of the project. Howard Shockey & Sons was the general contractor.

According to the City’s Revitalization Marketing presentation, the old assessed value of the property was $574,700 and after a $4.2M renovation, the new assessed value is $2,756,400. Along with historic rehabilitation tax credit incentives, the EDA provided below-market land conveyance.

Handley High School

The school recently went through a massive renovation project that cost about $72M. Depending on the source you look at, the project received anywhere from $2M to $5M to $10M in historic tax credits.

On November 24, 2010, Danielle Nadler reported for The Winchester Star that according to Winchester Public Schools Executive Director Kevin McKew, the project received $2,026,279 in historic tax credit funding. (This may refer to the cash received from the sale of tax credits to third-party investors.)

According to a 2010 convention document posted by the National Federation of Urban-Suburban School District (Charlottesville, Virginia), the project received $5M in historic tax credits.

TV3 Winchester reported the same number on October 4, 2009:

The project was funded through municipal bonds provided by the city and $5 million in historic tax credits.

However, according to an article in The Roanoake Times on October 3, 2010, that number was much higher:

In 1895, Judge John Handley left $1.6 million in a trust to the city of Winchester for education. John Handley High School opened with money from that gift almost 30 years later.

The historic school just completed a $72 million renovation and expansion project following a capital campaign, [Montgomery County school board member Joe] Ivers found in his research.

The school district hired a director of fundraising for three years to tap into its alumni base. It collected about $8 million, said Winchester schools Superintendent Ricky Leonard.

Mostly, the project was funded with $50 million from a bond on the city that required a property tax increase and about $10 million in historic tax credits.

The general contractor for the project was Howard Shockey & Sons.

George Washington Hotel

Like the Snapp Foundry rehabilitation, this project deserves an article all to its own. Maybe one will be posted soon. In the meantime, here is a summary…

According to the City of Winchester, the hotel renovations were completed in April 2008 for a total cost of $20.5M. The general contractor was G.W. Development LLC. For at least the next five years, if not ten years, the hotel’s increase in assessed value ($8.3M) will be exempt from real estate taxation. To help finance the project, developers received historic tax credits, New Market Tax Credits, and an EDA Business Development Grant.

A simple phone call to the Virginia Department of Historic Resources revealed that $5.3M in state historic tax credits were issued to the developer.

Based on information from the National Park Service (which involved a more complex phone call adventure), the final submitted rehabilitation cost eligible for the federal historic tax credit program was $21,542,325. The program issues tax credits for 20% of the cost, so that means the project received about $4.5M in federal historic tax credits.

According to the US Department of the Treasury, the New Market Tax Credit Program permits “individual and corporate investors to receive a tax credit against their Federal income tax return in exchange for making equity investments in specialized financial institutions called Community Development Entities (CDEs).”

The credit totals 39 percent of the original investment amount and is claimed over a period of seven years (five percent for each of the first three years, and six percent for each of the remaining four years). The investment in the CDE cannot be redeemed before the end of the seven-year period.

In turn, CDEs make loans and equity investments in commercial enterprises located in qualifying low-income rural and urban census tracts (Source):

“It’s a shallow subsidy if you just take it in the simplest form,” explains Joseph Flatley, CEO of Massachusetts Housing Investment Corp., which has closed several deals in which NMTCs were applied. “But it can be used within a leverage structure that can cover a significant portion of the project. For example, if you have a project with a million-dollar gap between what it costs and what it’s worth, NMTCs can fill that gap by 25 percent. So it’s a valuable tool.”

How many New Market Tax Credits were actually allotted for the project is not clear. Since the process is much more complicated and involves additional parties, an accurate figure is difficult to come up with at this point.

In addition, the City gives up a minimum of $280K in real estate tax revenue. That very conservative estimate is based on the 2009 property tax rate and 5 years of real estate tax abatement. It is not clear how long the real estate tax abatement lasts for the property. It is also not clear what the cost of the EDA Business Development Grant was for the project.

Lovett Building

The Lovett Building was built in 1900 and is located at 163-165 North Loudoun Street. Renovations on the building were completed in April 2010 by OakCrest Companies. The Lovett Building’s first floor now has office/retail space and one apartment, and the second and third floors have apartments. They are beautiful but a bit pricey: $900 per month for a one bedroom, one bathroom, 705 sq. ft. apartment.

According to Brian Wishneff & Associates’ official website, the cost for the Lovett Building project was $1M and the sale of historic tax credits reaped $300K.

James Heffernan reported for The Northern Virginia Daily (March 14, 2009):

OakCrest purchased the property in July 2005 for $525,000, and will put an estimated $600,000 into renovations.

The project will also take advantage of approximately $240,000 in historic tax credits through the Virginia Department of Historic Resources.

It is odd how OakCrest purchased the property for $525,000 and yet the City of Winchester’s “old assessed value” was $203,700. Anyway, according to the City, the new assessed value is $602,900 and the renovation and related costs were $295,000. It is not clear why the City’s numbers are not matching up to the numbers from the Wishneff group or The Northern Virginia Daily article.

In addition to the historic tax credits, this property became eligible for the City’s property tax abatement program.

Snapp Foundry Building

On June 29, the Winchester Watchdog wrote an exhaustive article, which has been recently updated, regarding the rehabilitation of the old Snapp Foundry building on North Cameron Street. The general contractor for the project was Howard Shockey & Sons.

To summarize, approximately $10M in tax credits went into the project. The property’s $2.5M increase in value is exempt from real estate taxes for a number of years. The City has a contract with the property owner for 15 years, paying $40,000 per month in rent for the Department of Social Services office.

Solenberger Co. Building

Prior to renovations, the City assessed the 142 North Loudoun Street property’s value at $372,600. According to an article in The Winchester Star by Vic Bradshaw (July 16, 2010), “Old Town Investments bought the [former Jno. S. Solenberger Co. hardware store] building in 2004 for $365,000, according to city records.”

Then, in July 2010, Shenandoah University paid $550,000 to Old Town Investments LLC for the property.

On February 24, 2011, Brian Wishneff & Associates reported that they had been “engaged by Shenandoah University to manage the tax credit process for its renovation of the historic Solenberger Building in downtown Winchester, Virginia into graduate student housing.” They list the sponsoring group as Shenandoah University and the estimated cost of the project at $3.5M. Apparently $1.3M in cash payment from the sale of historic tax credits has been received.

Howard Shockey & Sons Inc. was selected as the building contractor for the project. According to Shockey project manager Steve Knight, as reported by the Martinsburg Journal, the project would cost in excess of $2M and the University housing would be expected to open in August 2011.

In addition to historic tax credits, the property is eligible for the City’s property tax abatement program.

And last but not least…

Old Taylor Hotel

A full article about the hotel’s progress is available (click here), but this is an excerpt of the latest developments:

In January 2011, talks begin between City Council and Erik Wishneff regarding options for financing the renovation.

In March, according to The Winchester Star, a public-private partnership is proposed between the EDA and Taylor Hotel LLC for the $3.7M hotel rehabilitation project (which includes land acquisition) that could be partially funded with Community Development Block Grant money (at least $890,000 of it). Translation: taxes. The alternative–demolition–is estimated to cost $600,000.

After a closed meeting during their March 22 work session, City Council votes to forward an ordinance “to authorize the City Manager to execute the proposed agreement with the Winchester EDA for the redevelopment of the Taylor Hotel property and to take necessary acction to secure the I08 Loan in furtherance thereof, and allocate additional funding in the amount of $650,000.00 as a grant to the EDA to be used for the redevelopment of the property.” (Councilor John Willingham abstained from voting.)

According to The Winchester Star, the partnership would lease the pavilion and open space (what is currently the middle of the building) to the city for $42,500 annually until the commercial loan to be obtained to finance the property’s redevelopment is paid down to $600,000. Then the leased area would be conveyed to the city. The city would have to provide a $650,000 grant to the EDA for the project which would likely come out of reserve funds. Also, the partnership “will receive a Vacant Business Development Grant from the EDA – a refund of a portion of its tax payments. That money will be used to reduce debt.”

According to a March 26 article in The Winchester Star:

The $3.7 million project cost includes property acquisition, and [Jim] Deskins [executive director of the EDA and economic redevelopment director for the city] said that price might be renegotiated because the project has been scaled down from Wishneff’s initial plans.

The Wishneff group, which could not be reached for comment Friday, would provide $1.15 million for the project.

The city’s CDBG money would add another $1 million, and the city government would provide a $650,000 loan to the EDA to be used for the development.

The remaining $900,000 would be borrowed by a partnership to be formed between the EDA and the Wishneff group, with each side responsible for half of the loan.

According to the agreement, the Wishneff group would be responsible for any cost overruns.

On April 12, 2011, City Council hears the first reading of O-2011-11. According to City Attorney Anthony Williams, minor adjustments were made to this ordinance.

In May, City Council votes 8-0 to approve the public-private partnership for the rehabilitation of the Taylor Hotel. On May 16, The Northern Virginia Daily reported that according to the agreement “the developer, Wishneff LLC, and the EDA each will hold a 50 percent stake in the project.”

On June 30, The Winchester Starreports on another company expressing interest in purchasing the property should the Wishneff-EDA deal fall through:

Harry Gormas and Hunter Hurt, the architect who previously designed plans for the building for Lafayette Plaza LLC, have submitted a letter of intent to buy the historic structure if that deal fails and said they’re prepared to submit a backup contract.

Mr. Hurt is a member of the Board of Zoning Appeals and a past member of the Board of Architectural Review.

Presently, the Brian Wishneff & Associates website lists the Taylor Hotel as a current project with an estimated cost of $8M and a cash payment from sale of HTC of $2M. The website still lists Lafayette Square LLC as the sponsoring group.

So far it appears that at least $1.65M in tax dollars will go to the project — $1M in Community Development Block Grant money and a $650,000 loan from the City to eventually be repaid by the EDA. The EDA will also be responsible for repaying $450,000 in debt towards the project. Oddly enough, it appears that to pay down the loan amount, the EDA will issue the partnership (between Taylor Hotel LLC and the EDA) tax refunds. Perhaps that is an inaccurate interpretation, but the financing of the project is still as clear as mud.

Preservation through prosperity–is it real?

The Virginia Department of Historic Resources has a lovely PDF file titled “Prosperity through Preservation” that no doubt was incorporated on the local tour conducted this spring. The claim that rehabilitation projects create jobs resonates throughout the country. For example, Renee Kuhlman wrote for Forum News (April 2010):

Preservationists have made the point for years that rehabilitation projects create jobs at the local level and that state tax incentives make these projects economically feasible. Now new studies are supporting their arguments and lawmakers are paying attention.

“Historic preservation projects create jobs, especially in the manufacturing, retail trade, services, and construction sectors. In FY 2008, projects approved for federal tax credits had average budgets of $4.58 million and generated 55 jobs each,” claims the Advisory Council on Historic Preservation.

Richard Moe, president of the National Trust for Historic Preservation, wrote in 2009:

Nationally, there is overwhelming evidence that rehab tax credits are job-creators. Studying projects in Missouri, economist Donovan D. Rypkema found that 6.3 more jobs are created through rehabilitation than through manufacturing. Rutgers University also examined the impact of Missouri’s historic preservation tax credits and found that between 1998 and 2001, the state garnered 6,871 jobs and $60 million in tax revenues (including $25 million in state and local taxes) — an astonishing four-to-one return on the state’s investment in the tax-credit program.

But rehabilitation is typically not cost effective which is why most major historic building projects require massive tax credit incentives to encourage private investment. Without those tax credits, private investors would likely have put their money into some other venture, creating jobs there instead. What these folks are claiming, however, is that job numbers are created by tax credits rather than just shifted from one sector of the economy to another.

One can’t help but wonder if this isn’t all some fabulous example of the broken window fallacy. The idea that neglected, delapidated properties can be used to “create jobs” and boost the economy is one that stands on a rather shaky foundation. Based on this reasoning, it is better for the economy if someone allows their building to fall into ruin so that it can go through a massive, expensive renovation rather than spend the considerably smaller amount of money just maintaining the property every year. And common sense tells us that this simply isn’t true.

After researching the rehabilitation of the Snapp Foundry building, the fact that Brian Wishneff & Associates were involved in the Taylor Hotel rehabilitation attempts caught my attention. This company is an expert at utilizing tax credits to fund renovation efforts of designated historic properties. And these are the same folks in business with Councilor John Willingham.

The rehabilitation (and demolition) plans of the Taylor Hotel have been in the works for years. Note: this is not a restoration project.

2006

On March 15, the City of Winchester reports that the Taylor Hotel has been recently acquired. Plans for renovation include “a 60 room historic hotel, restaurant, and theater.”

2007

According to The Northern Virginia Daily, Lafayette Plaza LLC buys the property in October “with plans to convert it into a mix of upscale shops and condominiums.” The Property manager is Denver E. Quinnelly.

Taylor Hotel roof collapses on October 25.

Denver Quinnelly’s contracting firm Ricketts Construction Company Inc. goes “belly-up.”

2008

On April 23, 2008, the City of Winchester reports that the Hotel was “experiencing new life”:

Construction has begun and the new building will include condos and offices on the upper floors and retail space on the ground floor.

Denver Quinnelly settles lawsuit brought by the son of Ricketts Construction Company founder who claimed that Quinnelly “profited on both ends of the dealings between RCCI and his various development interests.”

2009

In March, the City fire marshal deems the building unsafe.

In April, a bank forecloses on seven of Denver Quinnelly’s unfinished subdivisions in Shenandoah and Frederick Counties. According to The Northern Virginia Daily, Springfield Financial Company “paid about $3.6 million to reacquire the properties from Taylor-Grace LLC, one of Quinnelly’s real estate development firms.” Taylor-Grace LLC owes Shenandoah and Frederick counties more than $60,000 in back taxes.

Perry Engineering files suit against Russell 150 LC (another company for which Quinnelly is listed as the registered agent) for breach of contract and $1.2 million owed for services, labor and materials provided to improve its mixed-use development project.

In a July 28 report local engineering firm Structural Concepts Inc. listed nine unsafe conditions of the building.

Denver Quinnelly chooses Ervin Construction Corporation to fix the problems including stabilizing the property’s partial roof, walls and balcony. According to The Northern Virginia Daily, he recommends razing two additions to the property and replacing them with a new building to connect to the front of the historic hotel, which would get a facelift.

The City agrees to accept a guarantee from Springfield Financial Company (Quinnelly’s lender) that would allow the spot blight abatement plan to go forward.

The City gives Lafayette Plaza LLC an August 28 deadline to submit a revised plan to rehabilitate the building or the City would “take action to declare it blighted.”

The City gives the company until September 26 to complete the emergency repair work.

By mid-September the City moves forward with plans to take over the property. James Heffernan reports for The Northern Virginia Daily (September 15, 2009):

In a letter to Quinnelly dated Sept. 9, and made available to the media on Monday, city Zoning and Inspections Administrator Vincent Diem says Quinnelly’s latest plans to demolish and remove the rear and middle portions of the building while stabilizing the hotel portion “will not render the building as being either fit or habitable [and] would not abate the blighting influence on the public’s welfare by retaining an empty shell of a historic landmark at the core of Old Town Winchester and within the Central Business District.”

The department of planning and zoning drafts a plan to begin stabilization work, acquire the property through eminent domain, and then start renovations using contractors or by selling it to another developer.

The Planning and Development Committee tabled the spot blight abatement ordinance for the property on September 22 and again on October 27.

On October 23, 2009 the City of Winchester reported that it had received a demolition permit for the Old Taylor Hotel. According to the plans prepared by R. Hunter Hurt, AI and submitted by Ervin Construction Corporation, certain portions of the existing structure would be demolished while other portions would remain stabilized and intact. According to the article, the demolition work was expected to begin as early as the following week.

2010

During a City Council work session on February 23, Mr. Diem reported that the emergency stabilization had been completed and the roof over the one story addition had been removed along with some mechanical items. However, it was the position of the Planning staff that the applicant had not performed within their timeline, and he aked that Council continue with the Spot Blight process. He also reported that correspondence had been received that day from the property owner stating that they were currently in negotiations for sale of the property. The Council unanimously voted to proceed with the Spot Blight plan.

On April 13 (and August 10), City declares the Taylor Hotel property “blighted.”

Erik Wishneff, of Brian Wishneff & Associates, signs a purchace contract for the building under the name Taylor Plaza LLC.

During the June 29 work session, City Council forwards two spot-blight abatement resolutions to the next meeting: approval of the Taylor Plaza plan for rehabilitation or demolition of the hotel.

Hotel problems remain: construction debris, rotting floors, fallen plaster, no roof, ineffective and corroded steel beams in an underground vault below the sidewalk

In August, City Council approves a resolution to accept the Taylor Plaza plan but authorizes demolition of the building if work is not begun. The resolution also requires the submittal of progress reports. Mr. Wishneff plans on using historic tax credits to help pay for the rehabilitation.

In October, The Winchester Star reports that “Erik Wishneff, a partner in potential buyer Taylor Hotel LLC” considers purchasing the property. (Harry Gormas is listed as the registered agent for this particular business.) According to the article, Taylor Hotel LLC was in talks with the Virginia Department of Historic Resources regarding federal and state historic tax credits for the project.

In November, The Winchester Star reports that “Taylor Plaza LLC is performing due diligence in hopes of buying the building from Lafayette Plaza LLC and redeveloping it.” (Not sure why the name of the company keeps changing–is it Taylor Plaza or Taylor Hotel?) Shenandoah Valley Discovery Museum considers purchase of the building.

2011

In January, talks begin between City Council and Erik Wishneff regarding options for financing the renovation.

In March, according to The Winchester Star, a public-private partnership is proposed between the EDA and Taylor Hotel LLC for the $3.7M hotel rehabilitation project (which includes land acquisition) that could be partially funded with Community Development Block Grant money (at least $890,000 of it). Translation: taxes. The alternative–demolition–is estimated to cost $600,000.

After a closed meeting during their March 22 work session, City Council votes to forward an ordinance “to authorize the City Manager to execute the proposed agreement with the Winchester EDA for the redevelopment of the Taylor Hotel property and to take necessary acction to secure the I08 Loan in furtherance thereof, and allocate additional funding in the amount of $650,000.00 as a grant to the EDA to be used for the redevelopment of the property.” (Councilor John Willingham abstained from voting.)

According to The Winchester Star, the partnership would lease the pavilion and open space (what is currently the middle of the building) to the city for $42,500 annually until the commercial loan to be obtained to finance the property’s redevelopment is paid down to $600,000. Then the leased area would be conveyed to the city. The city would have to provide a $650,000 grant to the EDA for the project which would likely come out of reserve funds. Also, the partnership “will receive a Vacant Business Development Grant from the EDA – a refund of a portion of its tax payments. That money will be used to reduce debt.”

According to a March 26 article in The Winchester Star:

The $3.7 million project cost includes property acquisition, and [Jim] Deskins [executive director of the EDA and economic redevelopment director for the city] said that price might be renegotiated because the project has been scaled down from Wishneff’s initial plans.

The Wishneff group, which could not be reached for comment Friday, would provide $1.15 million for the project.

The city’s CDBG money would add another $1 million, and the city government would provide a $650,000 loan to the EDA to be used for the development.

The remaining $900,000 would be borrowed by a partnership to be formed between the EDA and the Wishneff group, with each side responsible for half of the loan.

According to the agreement, the Wishneff group would be responsible for any cost overruns.

On April 12, 2011, City Council hears the first reading of O-2011-11. According to City Attorney Anthony Williams, minor adjustments were made to this ordinance.”

In May, City Council votes 8-0 to approve the public-private partnership for the rehabilitation of the Taylor Hotel. On May 16, The Northern Virginia Daily reported that according to the agreement “the developer, Wishneff LLC, and the EDA each will hold a 50 percent stake in the project.”

On June 30, The Winchester Starreports on another company expressing interest in purchasing the property should the Wishneff-EDA deal fall through:

Harry Gormas and Hunter Hurt, the architect who previously designed plans for the building for Lafayette Plaza LLC, have submitted a letter of intent to buy the historic structure if that deal fails and said they’re prepared to submit a backup contract.

Mr. Hurt is a member of the Board of Zoning Appeals and a past member of the Board of Architectural Review.

Presently, the Brian Wishneff & Associates website lists the Taylor Hotel as a current project with an estimated cost of $8M and a cash payment from sale of HTC of $2M. The website still lists Lafayette Square LLC as the sponsoring group.

So far it appears that at least $1.65M in tax dollars will go to the project — $1M in Community Development Block Grant money and a $650,000 loan from the City to eventually be repaid by the EDA. The EDA will also be responsible for repaying $450,000 in debt towards the project. Oddly enough, it appears that to pay down the loan amount, the EDA will issue the partnership (between Taylor Hotel LLC and the EDA) tax refunds. Perhaps that is an inaccurate interpretation, but the financing of the project is still as clear as mud.

Everything you could possibly want to know about it and then some…

The Winchester Watchdog hasn’t touched this because it didn’t look like it was needed. Various local media outlets have rigorously covered the debate, and citizens have actively engaged in the debate through local online and public forums. However, when readers request more information the WW typically will oblige.

One local resident asked, “Has anyone ever looked into the relationships that members of the planning commission and decision makers have with the University and Board of Trustees?”

Looking at relationships is very tedious and time consuming. And just because there appears to be a relationship on paper, it doesn’t mean there is one in reality. That being said, however, sometimes things will catch your eye and make you go “Hey, wait a minute…”

Local coverage and discussions on Millwood Proposal (Page 6)

Well, folks, it looks like this Millwood plan has been in the works for nearly a decade. Shenandoah University just had to wait for a more sympathetic City Council. According to Planning Director Tim Youmans, a previous effort to close the stretch of road in 2002 was met with opposition by the City Council, which approved a resolution specifically against it on December 10 of that year. But things changed in September 2009 with a Memorandum of Understanding between the City and Shenandoah University leaders. According to The Winchester Star, two of its points called for them to “work together on examining and improving traffic flow around the intersection and creating a new entrance to the city and university from Millwood Avenue.” Vic Bradshaw reported on May 13, 2010 in an article titled “Committee wants to study closing Millwood near SU“:

Creating a new entrance to Winchester and SU from Millwood and improving the traffic flow around Jubal Early and Millwood were two of the five projects city and SU officials had in mind when they signed a memorandum of understanding Sept. 21.

And on May 14, 2010, J.R. Williams reported for The Northern Virginia Daily:

Exploring the issue was among items in a memorandum of understanding between the city and the university recently approved by City Council. […]

City Planning Director Tim Youmans said using the stretch of Millwood solely for entrance to the university has been discussed.

“That’s just one idea,” he said, but the study will provide guidance. “City council said, before we go out and take action to close it, they wanted to have this traffic study done.”

The Traffic Study

On March 2, 2010, the Winchester-Frederick Metropolitan Planning Organization (Win-Fred MPO) Technical Advisory Committee (TAC) held a meeting that included a discussion on the Fiscal Year 2011 Unified Planning Work Program (UPWP) draft. During the discussion, Jerry Copp, VDOT maintenance manager for the Edinburg residency, reported that

he has attended several meetings with the University and the interim Winchester City Manager in regards to [the portion of Millwood Avenue located in front of Shenandoah University.] He stated that the University is proposing relocating the Millwood Avenue entrance. Mr. Copp stated that he received a letter from the Winchester City Manager requesting VDOT to perform a study. Mr. Copp stated that the cost of the study would be in the range of $75,000 and he has not been successful getting the approval from VDOT to perform the study.

It was obvious from the meeting minutes that MPO member Jim Deskins really wanted to see this study go forward, and considering that he has been working with SU President Tracy Fitzsimmons to increase the presence of Shenandoah University in Old Town Winchester, it’s no surprise. Mr. Deskins is also Executive Director of the Economic Development Authority for the City of Winchester.

During the TAC meeting, Mr. Deskins stated that the City is concerned with safety issues in the area and several other critical issues, not just related to Shenandoah University. His motion to forward a request to the Policy Board approving the use of local technical assistance funds to begin the RFP [Request for Proposal] process for the Millwood Avenue Study was approved by the committee. (A Request for Proposal is basically an invitation to companies to bid for a job, such as studying traffic patterns of a particular location.)

During the May 11, 2010 TAC meeting, Chris Price of the Northern Shenandoah Valley Regional Commission stated that the Policy Board requested that the TAC review the RFP and make a recommendation to them in May. He also stated that the deadline in the RFP would be changed.

At the May 19, 2010 Policy Board meeting, Mr. Price informed the group that the TAC had reviewed the RFP and recommended approval. Mr. Dehaven (who appears to be on the Project Steering Committee) requested that the Project Steering Committee lead the Study. Visitor Richard DeBergh asked how the project would be funded, and Mr. Price referred to the FY 2011 UPWP. He said that the study is a work task in the UPWP with a budget of $75,000. The RFP can be viewed here. Originally the consultants were tasked with only developing two scenarios: no improvements or access changes versus closure of Millwood Avenue.

On June 16, 2010 Mr. Price gave an update on the Study to the Policy Board. Thirteen proposals had been received and would be reviewed on June 30th by the Project Steering Committee who would decide on which consultants to interview.

A long discussion took place during the July 13, 2010 TAC meeting over the selection of Gorove/Slade since they were not the low bidder. According to Chris Price, the reason the Project Steering Committee chose that particular company was because “their presentation had the strongest stakeholder participation process and they made a point to recognize the University as a unique animal and thus needed to be treated as one.” He also discussed Gorove/Slade’s relevant project experience and references.

During the July 21 Policy Board meeting, Mr. Price gave an overview of the consultant selection process for the Study. Four of the proposals were submitted by local firms, and the lowest cost proposal was not interviewed due to errors and the scope of work did not conform to the request. John Willingham stated he would like the Board to use local firms as often as possible but the recommended firm was the leading selection. Richard Shickle expressed his concern in regards to the consultant selection process and subsequently voted against the motion approving Staff’s recommendation of Gorove/Slade Associates. Mr. Riley also voted against the motion.

The study was completed near the end of 2010, and a final draft can be viewed here at the Win-Fred MPO website.

One thing made perfectly clear was that “Safety was stressed by all stakeholders as the primary focus.” Considering that the entire reason for the Study was to determine the short- and long-term traffic impacts associated with the proposed closure, let’s look at that, shall we?

According to the Study, “the potential closure of Millwood Avenue could impact traffic flow on the commuter route between the I-81 Interchange or arterial streets east of the City and downtown Winchester.” Also, “the amount of traffic that uses Millwood Avenue between Jubal Early Drive and Apple Blossom Drive is significant, representing 44% of the traffic traveling into the City on Millwood Avenue. A slightly less percentage is seen in the reverse movement from downtown towards the East. The evening split is not as high to downtown, which is likely due to the influence of retail-based traffic on overall traffic patterns.”

When looking at key intersections, the Study found that “the potential closure of Millwood Avenue could lead to increases in delay at these key intersections, since a significant amount of drivers travelling toward downtown use the section under the study.”

During commuter peak hours, a Level of Service grade of “E” is considered to be at capacity and “F” is considered unacceptable:

Well, what about pedestrians?

According to the Study,

The amount of pedestrians crossing the area along the stretch of Millwood Avenue under consideration for closure was not collected, as observations indicate that few pedestrians cross in this area.

What about car accidents?

The crash data shows that the vast majority of crashes occur at intersections, with rear end collisions representing the majority of accident types. No pedestrian or fatal accidents were among the police reports provided by the City.

The highest intersection crash rates were at Millwood Avenue/Pleasant Valley Road with 3 crashes per million entering vehicles and Jubal Early Drive/Pleasant Valley Road with 2 crashes per million entering vehicles. According to the Study, “transportation engineers consider a crash rate over 1.0 a concern and over 2.0 as a significantly high rate where further study is needed.”

The principal crashes at these intersections are rear end collisions. This is typical at signalized intersections, where rear end collisions are a large percentage of the total crashes. Rear end collisions are generally caused by following too closely or by driver distraction. Speed certainly plays a factor in rear end collisions as the higher the speed, the larger the following distance that is required to stop without collision and the greater the potential severity of the crash.

Left turn crashes are the next highest crash type at these intersections. Failure to yield was noted in many of the crash reports as the reason for the crash. The skewed geometry of the Millwood Avenue/Pleasant Valley Road intersection could be a factor in the very high crash rate at this intersection. Skewed geometry results in longer turning distances, so turning vehicles are in the path of oncoming traffic longer and turning drivers may misjudge the appropriateness of the gap in oncoming traffic for making the turn. For this reason, along with others, skewed intersection geometry should be avoided.

Most crashes in the study area occurred at the intersections outside of the immediate area of the Millwood Avenue section contemplated for closure. The crash history showed nine total crashes during the 2006 to 2009 period at Millwood Avenue/Apple Blossom Drive with a rate of 0.5.

Based on the computer simulation, the intersection at Hampton Inn & Millwood Ave will be far worse under the proposed closure, now and in 2035. The intersection at Jubal Early Dr & Apple Blossom Dr will presumably be better under the proposed closure, but that assumes the closure will include signal timing improvements at the intersection in conjunction with the addition of the free-flow right-turn lane. Also the 2035 projection assumes that the signalized intersections in the study area would be retimed in order to account for future projected growth. How much better would the intersections be if the City kept Millwood Avenue open while still improving signal timing and adding a free-flow right-turn lane?

Common sense tells us that the more cars you cram in an area with less alternatives, the more congested remaining intersections and roads will get. Perhaps the authors of an editorial piece in The Winchester Star put it best when they wrote:

Blocking Millwood, we admit, will reduce confusion – and, perhaps, accidents – at the I-81 “chokepoint” near the Bob Evans Restaurant by funneling all traffic onto Jubal Early. On the other hand, the elimination of Millwood as an option – a safe option, may we add, comparatively accident-free – means all 36,000 cars passing through that intersection each day will be obliged to travel on Jubal Early where more accidents have occurred. What’s the advantage, in terms of safety and traffic flow, to placing all such vehicles onto Jubal Early?

There seems to be this false dichotomy in the Study that either something is done with Millwood and improvements are made elsewhere or nothing is done with Millwood and no improvements are made elsewhere. Obviously this was done on purpose by the folks who commissioned the Study in the first place.

How about keeping Millwood open and making needed improvements to intersections on Jubal Early, Apple Blossom, and Pleasant Valley? But that would mean Shenandoah University would not be able to acquire public land for its private use.

Changing Tactics

As was already shown, the stated primary purpose of the traffic study was safety. This was confirmed in public news and discussion. For example, Christopher Bean of Stephen City, (maybe the same Christopher Bean who is Director of Shenandoah University’s Libraries?) wrote in a Letter to the Editor of The Winchester Star on February 11, 2011:

The primary reason for considering the relocation of Millwood Avenue is traffic safety. No amount of directional signage or speed limit signs is going to alleviate the problem with this very confusing and dangerous roadway.

And on April 6, 2011, Alex Bridges reported for The Northern Virginia Daily:

“The overall takeaway from all this, we’re looking beyond just a delay and level of service for vehicles,” said Tim Youmans, Winchester’s planning director. “We’re basically saying we want to create a safer situation, and certainly the traffic light at the Hampton Inn-Beltone location provides for the safe pedestrian-bike movement for the university students and what will hopefully be a growing number of people using the Green Circle trial.”

On April 22, 2011, The Winchester Star published an article titled “SU plans gateway entrance to school,” but Jim Vickers, the chairman of SU’s Board of Trustees, was adamant that safety was the number one priority:

While aesthetic improvements are envisioned, Vickers said the SU trustees’ main concern is vehicular and pedestrian safety.

[…]

“The driving point, the major concern, always has been safety for pedestrians and cars,” he said. “That’s a concern for the university and the city.”

But the traffic study clearly showed that pedestrian safety is not a problem on that stretch of Millwood Avenue. Vehicular safety is also not a problem on that stretch of road. In fact, it is a much safer alternative to taking Jubal Early Drive.

The SU President, however, thinks otherwise. On June 11, 2011, Alex Bridges reported for The Northern Virginia Daily:

SU President Tracy Fitzsimmons spoke to local media at her office Friday afternoon and released new renderings by architectural firm Van Yahres Associates that depict how the area targeted for closure may appear should the city approve the proposal.

Officials have expressed concerns about the safety of pedestrians walking from the Vickers Communication Center to the area of the Ohrstrom-Bryant Theatre.

“That’s the part of Millwood Avenue that’s really a raceway,” Fitzsimmons said.

In addition to solving the traffic and safety issue, the architectural firm sought to create “a more aesthetically pleasing, inviting, beautiful entrance to Winchester and the university,” Fitzsimmons said.

“You should first be welcomed to the city,” Fitzsimmons said. “When you get to the entrance of the university you should be welcomed to the institution.”

And in a Letter to the Editor of The Winchester Star on June 20, 2011, SU Trustee CJ (Carol) Borden wrote:

Safety of SU students is my main concern. SU now has students who live across Millwood Avenue from the main campus, and with the converging of roads, it is an unsafe area for SU students to cross over to the main campus.

In addition, entering Winchester from I-81 onto Route 50W, from the viewpoint of a stranger to the area, is not an attractive entrance, and definitely not a welcoming one. By closing Millwood, a much more attractive entrance could be designed.

As became increasingly clear in the local news this spring and summer, the focus was less on safety and more on asthetics. Yes, safety remained a “goal” (although there is no evidence that safety has ever been a problem on that stretch of Millwood Avenue), but now the big push is for a “grand entrance” to the City, and particularly for the University.

[Vice President for the Advancement of SU, Mitch] Moore says having a more attractive entrance and allowing the University to prosper allows the city to prosper as well.

Even a City Planning Commissioner felt the need to comment on the motives behind the Millwood proposal. Alex Bridges reported for The Northern Virginia Daily (July 2, 2011):

Planning Commission Chairman Nate L. Adams III questioned the motive and need to close the section of Millwood Avenue just to improve the entrance to the city. [SU Board of Trustees Chairman Jim] Vickers acknowledged the university could do so without closing Millwood, but he said the result would be less appealing.

It is obvious what has happened here: the City and the University have planned to close Millwood for nearly two years and they simply wanted to find justification that was palatable enough for the public to accept.

As I am sure most of my readers are well aware, the front page of the Winchester Star on Saturday (July 2) featured an article about the “reassessment battle” in the City of Winchester.

Thank you, Mr. Bradshaw, for reporting on this important story.

One interesting little tidbit caught my eye:

[City Council President Jeff] Buettner said that when new property valuations were sent to residents, he fielded concerns from citizens about commercial and residential properties, as is the case with every reassessment.

He said he spoke with Rice about the valuation of his business property, Buettner Tire, and asked for a meeting.

However, he said he canceled the meeting because he “didn’t want there to appear to be a conflict of interest” and accepted the valuation.

Rice confirmed talking with Buettner about the matter and that the council president canceled their meeting. He said Buettner did not appeal the valuation to the Board of Equalization.

Seeing as how the Winchester Watchdog is just a “tabloid” that “harasses” the City, I have decided to beat the dead horse one last time and point out some issues I saw with City quotes in the Star article.

According to The Winchester Star, when the Commissioner of the Revenue asked the City Manager why the local government wanted to change the reassessment process,

she said he told her he understood that the assessor was not part of her office.

Maybe not, but according to the official City of Winchester website, it sure does appear to be:

In fact, the City, if this proposed change goes through, will likely have to rewrite the entire Chapter 27 of the City Code because the Assessor and the Commissioner of the Revenue are often required to “work jointly” on tax assessment issues.

I suspect that there are a variety of reasons for the change, not the least of which is the fact that the City wants more revenue.

The Star also reported on Saturday that “Buettner said … the council has not had in-depth, formal discussions about the issue.”

What a load of baloney!

I came across a March 30, 2011 article in the Winchester Star written by Vic Bradshaw titled “City on quest to find $50,000 for lagging department needs” and noticed that the tax reassessment process was briefly mentioned, including the position of city assessor:

Councilors also discussed the philosophy of performing inhouse mass reassessments of real estate, a task performed every two years, or contracting out for those services. Their decision will affect the budget regularly on multiple levels, including the role of the city assessor.

The 2010 mass reassessment was done by Commissioner of the Revenue Ann Burkholder’s office. But Buettner, Major and Vice Mayor Milt McInturff said they favor having a third party with no financial stake perform the biennial re-evaluation of real estate values.

That article was published two weeks after the City Assessor was told by the City Manager that his position was likely to be eliminated.

Check out this excerpt from the March 29 City Council Budget Work Session minutes [emphasis mine]:

City Manager James O’Connor stated the budget was developed under the premise of no tax increase, a balanced budget, level funding for schools, outside agency funding reflective of Council goals/mission statement and similar to last year’s funding, and the maintenance of existing service levels. There are two issues that the administration needs Council direction tonight. First is the tax assessment process as we move forward. The question is do we want to do the next assessment in house or by contractor. We have the opportunity to make the decision to either invest in needed software or prepare an RFP to seek outside services. We also have the opportunity to redefine the position of Tax Assessor depending on how Council wants to proceed. If the reassessments are done in house, the qualifications of the Tax Assessor would be different than if the assessments are contracted out. He asked if Council would like staff to proceed and come back with options or give direction tonight. Staff is on the verge of needing to purchase software ranging from $59,000 to $100,000 to be timely for the next assessment.

After a brief discussion on the benefits of the transparency of an independent, contracted professional, Council directed Mr. O’Connor to pursue the opportunity to go in on an RFP with Warren, Page and Shenandoah Counties and come back with options.

President Buettner stated he would like to see a proposal of what staff feels is the best way to redefine the Tax Assessor position and if an ordinance would be needed.

Then, during the Common Council work session on May 24, Council members unanimously approved by voice-vote that the new ordinance be forwarded to Council. Evan Clark, who claimed in March that “he’d like to see a cost comparison of the two methods before deciding how to proceed” was the one to second Art Major’s motion.

Remember, a cost comparison has shown that the in-house reassessment by the Commissioner of the Revenue’s office and the City Assessor was less expensive and more accurate than previous reassessments by third parties, and on Saturday The Star also reported that in-house reassessment is common in cities the size of Winchester.

Seriously, Mr. Buettner, how do you vote on a motion regarding a proposed ordinance without any “formal discussion”? And wasn’t the proposed ordinance part of the City Council’s agenda for the June 14th meeting?

One thing that I wish The Star article had investigated further was the fact that the City Council is trying to put the reassessment responsibility under the Finance Department. If all the Council cared about was having third-party reassessments, the Commissioner of the Revenue could easily continue to oversee the process. But instead they want to put reassessments directly under the control of the Finance Department and the City Manager.

And we still don’t know why.

Update (July 6):

Ann Burkholder took exception to the approach of the Winchester Star towards the reassessment discussion taking place in the city government.

She wrote a response to the article in question in the Winchester Star‘s Open Forum section titled “Battle in City Hall?” (July 6, 2011). She concluded beautifully with this:

Finally, by using the term “battle” and juxtaposing our photos, The Star implies that Council President Jeff Buettner and I are locked in a feud. This is certainly not my understanding. The record of accomplishments over the past 18 months shows that the commissioner and council have worked cooperatively to clean up discrepancies in City Code, implement new state laws, and address a number of long-standing issues, each to our citizens’ betterment.

We have seen at all levels of government that once elected officials become polarized, nothing productive happens. Our citizens deserve effective leadership, and I am committed to that goal.

And people call the Winchester Watchdog a “tabloid”!

(I still think the Council has been shady on this issue.)

As was discussed in the earlier post “City proposes changes to tax assessment process“, in a formal document overloaded with the word “WHEREAS”, the City Council has provided explanations for the proposed changes. But as was also discussed, these reasons don’t make a lot of sense.

This document was not previously included because it is easy for readers to “get lost” in it, but now I think it is important. From page 153 of the June 14 Agenda (skip it if your eyes start to cross) :

AN ORDINANCE TO AMEND AND RE-ADOPT SECITON 27-10.1 OF THE WINCHESTER C1TY CODE REGARDING BIENNIAL REASSESSMENTS

WHEREAS, the City of Winchester currently performs biennial reassessments and equalization of real estate in accordance with Sections 27-10 and 27-10.1 of the City Code; and

WHEREAS, such reassessments had historically been performed in the City of Winchester by an outside contractor; and

WHEREAS, such reassessments were performed “in-house” under the management and supervision of the City Assessor for the first time this year; and

WHEREAS, the City Assessor position was vacated in April of 2011 when the City Assessor resigned and his position currently remains unfilled; and

WHEREAS, it is the belief of Common Council that the use of a private contractor to conduct biennial reassessments would likely be the most effective and efficient way to ensure that reassessments are conducted thoroughly and uniformly given the current vacancy; and

WHEREAS, it is further the belief of Common Council that the management and oversight of the private contractor would best be handled by an in-house employee with experience in managing such contracts such position being hereinafter referred to as the “Real Estate Administrator”; and

WHEREAS, it is the belief of Common Council that no formal request or delegation pursuant to §581-3270 of the Code of Virginia to the Commissioner of the Revenue has been made to perform assessments on behalf of the City and that if such a request or delegation is otherwise construed to have been made it should be revoked and rescinded; and

WHEREAS, §58.1-3275 of the Code of Virginia specifically provides that the general reassessment of real estate in a city or county can be performed by an independent contractor holding a certification issued by the Virginia Department of Taxation; and

WHEREAS, the provisions for biennial reassessments are set forth under Article II, Division 1 Sections 27-10 through 27-10.1 of the Winchester City Code.

NOW therefore be it ORDAINED, that any prior action of this governing body which could be construed as a request or delegation to the Office of the Commissioner of the Revenue pursuant to §58.1-3270 of the Code of Virginia or similar law to perform assessments or reassessments on behalf of the City is hereby revoked and rescinded. Be it FURTHER ORDAINED that Section 27-10.1 of the Winchester City Code is hereby amended and re-adopted as follows: SECTION 27-10.1. AUTHORIZED.

Additionally,

According to the proposed ordinance, a “Real Estate Administrator” shall be appointed by the City Manager and come under the direct supervision of the Finance Director. The Administrator shall be responsible for ensuring that the contractor satisfies all contractual requirements and complies with all applicable provisions of the Code of Virginia and general law with regard to the performance of the reassessments. Council may from time to time authorize the City to employ such assistants as deemed necessary to aid the Administrator in the performance of his duties.

See? It’s a pain to read. But, the key part is this:

WHEREAS, the City Assessor position was vacated in April of 2011 when the City Assessor resigned and his position currently remains unfilled; and

WHEREAS, it is the belief of Common Council that the use of a private contractor to conduct biennial reassessments would likely be the most effective and efficient way to ensure that reassessments are conducted thoroughly and uniformly given the current vacancy; and

WHEREAS, it is further the belief of Common Council that the management and oversight of the private contractor would best be handled by an in-house employee with experience in managing such contracts such position being hereinafter referred to as the “Real Estate Administrator”;

According to Mr. Will Rice, the former City Assessor, the explanation that that the City wants to change the department for the responsibility of tax reassessment because the assessor resigned “is false”:

I was told by the city manager that my position was going to be changed before I resigned. I was told that I would have to reapply for my job. This was before this all became public. This change was not caused by my resignation, my resignation was caused by this change being presented to me.

So why the change, City Council?

(You have no idea how hard it is to get an answer in writing to this question. Emails questioning the proposed change in tax assessment were sent last Thursday to City Manager Jim O’Connor, Finance Director Mary Blowe, Council President Jeff Buettner, Councilor John Willingham, and Councilor Art Major. No replies have been received as of June 29 except from Mr. Buettner who promised to reply once he returns from vacation on July 5th. It is not clear whether the emails were simply not received or if they are being ignored. After all, they were sent from the Winchester Watchdog email address. Additional emails have now been sent to the remaining Council members and the Mayor.)

Mr. Rice also wrote:

I was told that they were planning this change and that I would have to reapply for my job March 14. Once that statement was made to me I decided to look at other options for employment. I have a wife and a 5 year old daughter that I have to look after. I was not willing to take a risk on the possibility of not being rehired. This was a very hard decision for us to make.

Mr. Rice is presently, and happily I might add, employed with the City of Chesapeake where he recently moved with his wife and young daughter. Even though he was “caught off-guard by the manner in which things occurred,” Mr. Rice is certainly not a disgruntled employee, and he loves the Winchester area.

“I was not raised in Winchester,” he said. “However, I came to Winchester in 1999 and attended Shenandoah University for Poli/Sci and Public Administration and fell in love with the area. I interned for the City in both the Administration Department and the Assessor’s office. It was the place where I learned about the function of the Assessor’s office and decided that was what I wanted to build a career in. Unfortunately I was not able to obtain a position there right after college. However 4 years later I was fortunate enough to be hired as the Assessor and was able to come back to an area I loved. My wife and I decided we would love to raise our family here and were excited about the opportunity to be involved in such a great small community.”

The Commissioner of the Revenue, Ann Burkholder, has independently confirmed the sequence of events.

In March, the City informed the Asssessor that his position was going to be eliminated and he would have to reapply for employment with the Finance Department, thus effectively eliminating the Assessor position prior to actually passing an ordinance. Then, the City used the vacancy as an excuse for the ordinance now being proposed.

Note: As Council members and other city officials reply to requests for information, this post will be updated with their responses.

Note: Scroll below for updates interspersed throughout the article. Last update July 8, 2011.

Several readers have recently asked about the $40K/month rental situation of the Department of Social Services office at 24 Baker St. that was mentioned in Winchester Watchdog’s very first newsletter. This article provides a basic timeline of events regarding the Our Health Community Campus on North Cameron Street, and it includes information about the companies involved in the property sales, renovation and rental income.

One reader forwarded correspondence from Councilor Evan Clark regarding the Social Services’ rent of the renovated Snapp Foundry building. According to that correspondence, the contract negotiations “began well before John [Willingham] was elected.” The City “had several options to choose from and the former location needed millions of dollars to be ADA compliant, and even then it was not big enough.” He also wrote that “the old building needed HVAC plumbing, electric and I think a roof. Long story short, the other options sucked. They were more expensive, and they were too small.”

The Frederick/Winchester Health Department is located at 10 Baker Street which is owned by the same company that owns 24 Baker Street: North Cameron Properties LLC (NCP).

Council member John Willingham’s 2010 Statement of Economic Interests states that “North Cameron leases space to City of Winchester” and the “City of Winchester leases [illegible] of this space to Virginia.” Mr. Willingham owns “33% of it in an LLC which has majority ownership of NCP.” That LLC is probably OTSS.